Investing in digital assets brings complex legislative obligations in addition to high profits. Many investors are looking for legal ways how to avoid paying crypto taxes without violating the valid laws of the Slovak Republic. The key to success is not concealing income, but strategic planning, precise accounting, and using legitimate tools that the state directly offers to investors. A properly optimized portfolio can legally reduce the tax burden down to zero.

What does Slovak legislation say about the taxation of digital assets?

The taxation of digital assets in Slovakia is a process where the income from the sale or exchange of virtual currency is considered other income according to § 8 of the Income Tax Act. The taxable moment is not only the sale of cryptocurrency for fiat currency but also its exchange for another cryptocurrency, a stablecoin, goods, or provided service.

According to the Income Tax Act No. 595/2003 Coll., virtual currency is defined as a digital bearer of value. If you realize a profit from trading, you must include it in your tax return. Professional tax advisory will help you correctly determine the tax base and identify all deductible tax expenses.

When calculating the net profit, the principle of assigning real expenses for acquisition to a specific sale applies. Without consistent transaction records, there is a risk that the financial administration will not recognize your costs, leading to unnecessarily high and inefficient taxation.

How to avoid paying crypto taxes legally using tax exemption?

The exemption from crypto taxes is a legislative mechanism that allows natural persons to legally not pay income tax and health insurance contributions from the sale of virtual currencies. The condition is the successful fulfillment of legally defined time criteria between the purchase and the subsequent sale of a specific digital asset.

The Slovak tax system makes it possible to eliminate the tax obligation through an exemption if the investor follows exact asset holding rules. The use of this exemption requires flawless time pairing of purchases and sales, which can be problematic with hundreds of transactions. To minimize the risk of errors, it is optimal to entrust the tax return processing to licensed specialists.

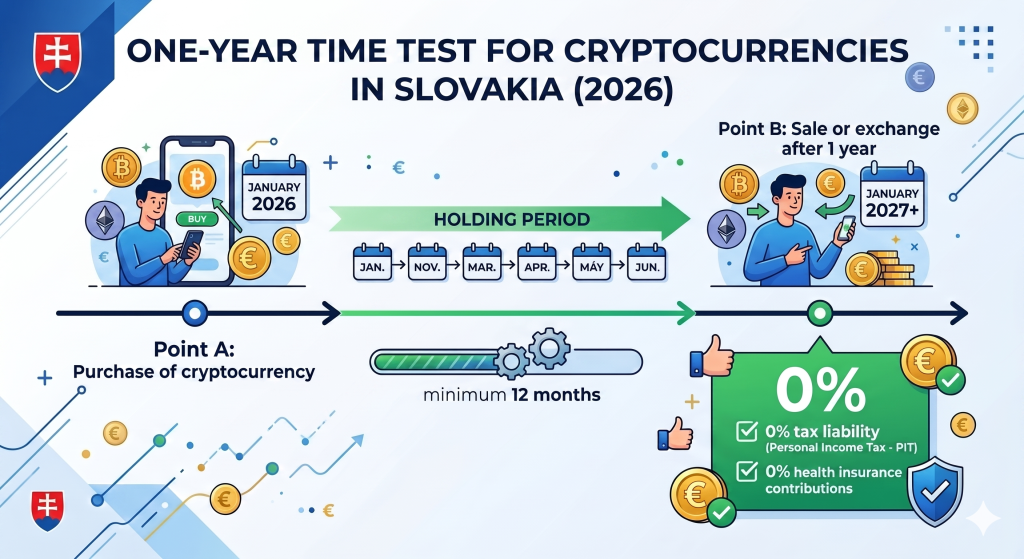

When does the time test for income tax exemption apply?

The time test is a legally established period of 12 months during which the taxpayer must continuously own the cryptocurrency in order for the income from its sale to be completely exempt from tax. If the sale or exchange occurs only after one year from acquisition, the achieved income is not subject to taxation or contributions.

According to the legislative framework valid in 2026, long-term investors are subject to the so-called one-year time test. If you buy Bitcoin or another cryptocurrency and sell it at the earliest after one year, the achieved capital gain is fully exempt from personal income tax. This mechanism represents the most effective way how to avoid paying crypto taxes in Slovakia in accordance with the law.

It is important to note that any interim exchange of assets (for example, BTC for ETH or a stablecoin) during this one year interrupts the time test and immediately triggers a tax obligation.

What are the most common mistakes and risks when optimizing a crypto portfolio?

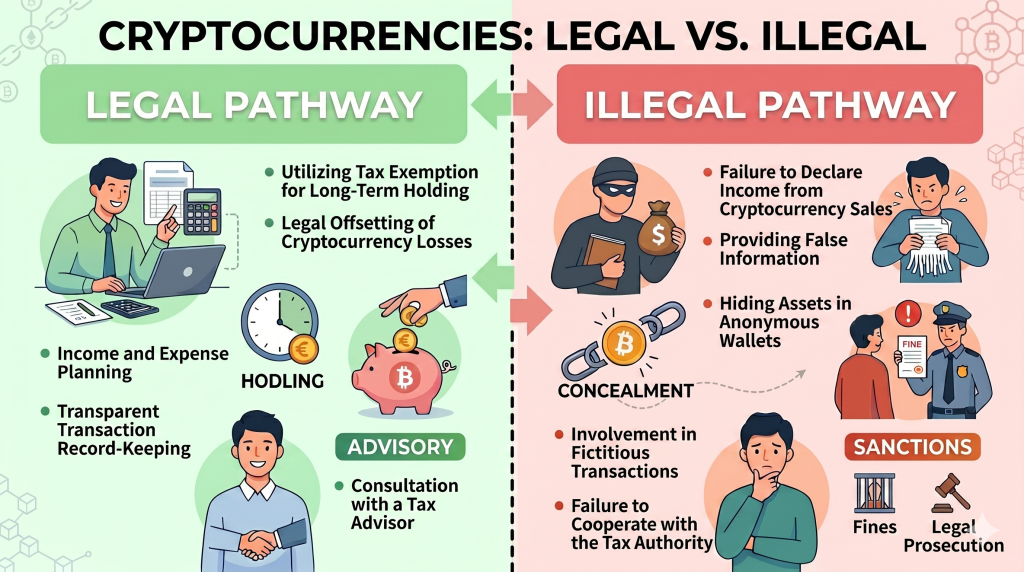

Crypto portfolio optimization is a legal process of minimizing the tax burden using strategic planning and utilizing valid laws. The most common mistake of investors is confusing this legitimate activity with illegal tax evasion, such as concealing wallet addresses or intentionally not declaring profits.

Many traders mistakenly believe that decentralized exchanges and non-custodial wallets guarantee absolute transaction anonymity. If an investor moves their funds through a centralized exchange with identity verification, every subsequent transaction on the blockchain leaves a permanent and publicly traceable digital footprint. Financial institutions and state authorities today commonly use advanced analytical software to retrospectively track the flow of capital.

Among other critical failures in practice belong:

- Absence of continuous records, where the investor cannot retrospectively and credibly prove the acquisition price of the assets.

- Misunderstanding of stablecoins, where exchanging volatility for a fixed exchange rate is considered a taxable moment.

- Ignoring transaction fees, which can serve as a legitimate tax expense reducing profit.

What are the consequences of not paying taxes on cryptocurrencies and how does the financial administration’s control work?

Not paying crypto taxes is a violation of tax regulations that occurs if the taxpayer intentionally or negligently fails to include income from digital assets in the tax return. The Financial Administration of the Slovak Republic identifies this offense through international data exchange and imposes strict financial and criminal penalties for it.

If there is a discovery of income reduction, the tax office will retrospectively assess the tax and levy a fine in the amount of default interest. Intentional non-payment of crypto taxes on a larger scale fulfills the elements of the criminal offense of tax and insurance evasion under the valid Criminal Code. In 2026, control mechanisms are interconnected with the banking sector, meaning that suspicious deposits to a personal account automatically trigger a local investigation.

How to legally minimize the tax obligation when trading cryptocurrencies?

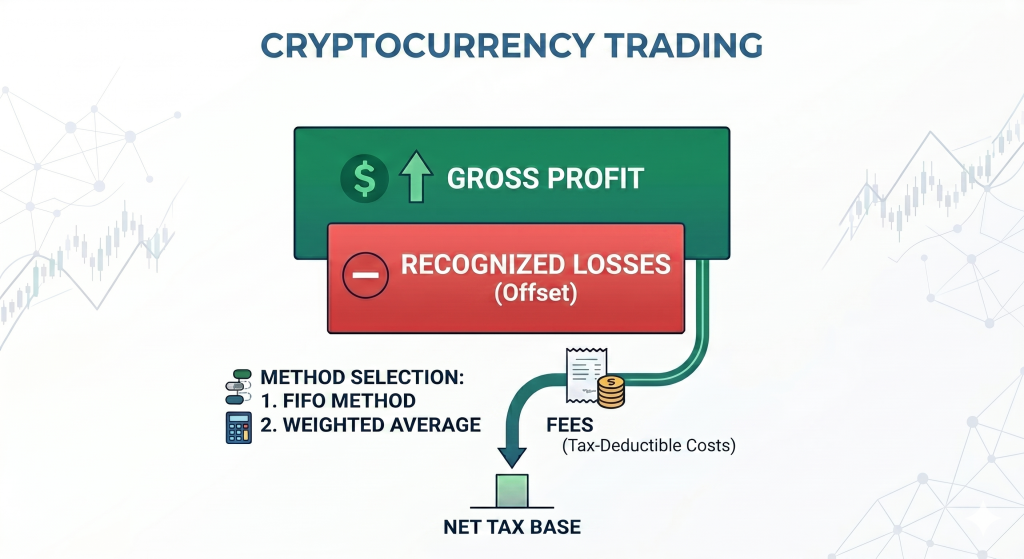

Minimization of tax liability in trading is a legitimate accounting strategy of reducing the net tax base by applying actual expenses and optimization methods. This procedure involves the precise pairing of losses and gains within a single tax period in order to report the real economic result.

If you actively trade, the key to success is the FIFO method or the weighted average method in valuing cryptocurrency inventory. By making the right choice of accounting methodology, you can legally compensate for profitable trades with losing ones, effectively compressing the resulting tax base. All fees associated with the purchase, sale, or transfer of digital assets are considered a tax-deductible cost.

Is it worth transferring crypto assets to an LLC (s.r.o.) or using foreign jurisdictions?

Transferring crypto assets to an LLC (s.r.o.) is a strategic decision where the holding and trading of virtual currencies is carried out by a legal entity instead of a natural person. This step completely changes the tax regime, as a limited liability company is subject to different tax rates and contribution obligations than an ordinary citizen.

If you are considering moving capital into a company, you must carefully compare the corporate income tax rates with the progressive taxation of natural persons. Legal entities cannot use the one-year time test for tax exemption, which is a major disadvantage for long-term investors. Using foreign jurisdictions is subject to strict rules on controlled foreign companies, which prevent the illegal siphoning of profits.

|

Comparison parameter |

Natural Person (Individual) |

Legal Entity (LLC / s.r.o.) |

|---|---|---|

|

Basic tax rate |

19% or 25% |

15% or 21% |

|

One-year time test (exemption) |

Yes (0% tax after 1 year) |

No (always taxed) |

|

Health insurance contributions |

Exempt with time test |

No (tax paid from dividends) |

|

Application of crypto losses |

Limited within the law |

Possible within the tax result |

What will be the future development of cryptocurrency taxation under the influence of European regulations?

The future development of cryptocurrency taxation is a legislative process of tightening global supervision, which, through the European DAC8 and MiCA directives, introduces fully automated information exchange between crypto platforms and tax authorities of member states. This step definitively eliminates the previous apparent anonymity and brings absolute transparency to the entire ecosystem of digital assets.

The implementation of European rules will fundamentally change the way state authorities approach inactive or undeclared crypto accounts. Tax authorities will gain direct and immediate access to historical transaction data of all Slovak tax residents on foreign centralized exchanges. If an investor has so far considered risky tactics, such as the intentional non-payment of crypto taxes, after the full deployment of these integration systems, such conduct will be immediately identified. The increased level of control, however, will also bring much clearer rules for institutional investors and overall market stabilization on the other hand.

Summary: How to approach cryptocurrency management in 2026?

Crypto portfolio management in 2026 strictly requires consistent compliance with the legislative framework and proactive use of all available legal tools. The safest way how to avoid paying crypto taxes in Slovakia remains the strict application of the one-year time test for natural persons, along with precise recording of every single executed transaction.

Legal optimization represents the only long-term sustainable way to effectively protect your achieved profits from liquidating financial penalties. Regular consultation with certified tax experts minimizes any risk of errors when filing a tax return. Forget about old myths concerning the untraceability of transactions on the blockchain, and instead choose a transparent, completely legal path that will guarantee the stability and safe growth of your digital wealth.

Expert FAQ Section (Frequently Asked Questions)

Do I have to pay tax if I only exchange one cryptocurrency for another?

Yes, according to current Slovak legislation, the exchange of one virtual currency for another (for example, exchanging Bitcoin for Ethereum or a stablecoin) is considered a regular taxable moment. In such a case, you are obliged to calculate the positive difference between the acquisition price of the original asset and the fair market value of the new cryptocurrency at the exact time of the exchange, and declare this profit.

What are the penalties if a taxpayer intentionally conceals income from crypto assets?

Intentional non-payment of crypto taxes leads, upon discovery, to the immediate initiation of a tax audit, retrospective assessment of the entire tax amount, and the imposition of a severe fine in the form of default interest. If the total scale of this income evasion exceeds the legally established threshold, this behavior fulfills the elements of the criminal offense of tax and insurance evasion.

Does the one-year time test also apply to staking or cryptocurrency airdrops?

No, the legislative one-year time test for full tax exemption applies exclusively to realized capital gains from the classic sale or direct exchange of the cryptocurrency itself after 12 months of continuous holding. Regular income derived from staking or free airdrops is considered a different type of income, which is subject to taxation at the moment it is credited to your wallet.