The establishment and operation of a limited liability company brings strict legislative obligations in the area of financial management. The question of how to manage bookkeeping in an s.r.o. efficiently and without sanction risks is crucial for every statutory representative, who bears full legal responsibility for the accuracy of economic results. Properly set up financial management minimizes exposure to tax audits and ensures exact data for strategic decision-making. The company Lukáčik & Partners provides corporate clients with highly professional bookkeeping management, which transforms the administrative burden into a strategic advantage.

What kind of bookkeeping does an s.r.o. maintain by law?

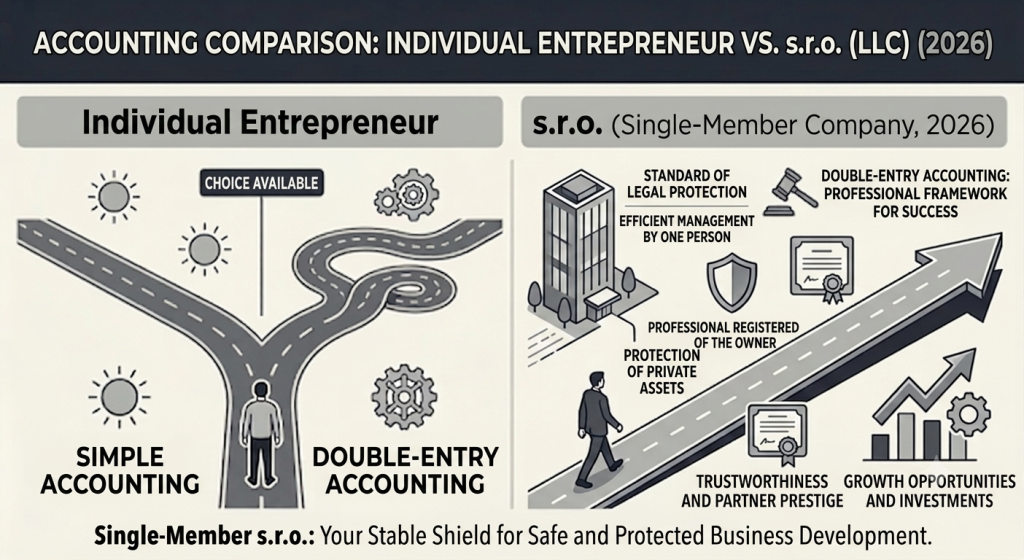

A limited liability company is a corporate business entity that, according to valid Slovak legislation, has a categorical obligation to maintain double-entry bookkeeping. This system represents a comprehensive method of continuously recording the state, movement, and financial result, while strictly separating the company’s assets from the personal finances of the partners.

According to the Ministry of Finance of the Slovak Republic, this obligation is absolute from the moment of the company’s incorporation in the Commercial Register until its dissolution. Unlike natural persons – entrepreneurs, legal entities do not have the option to choose tax records. If you analyze what kind of bookkeeping an s.r.o. maintains, the legislation does not allow any exceptions based on the turnover amount or the number of employees.

What exactly does the Accounting Act define for business companies?

Act No. 431/2002 Coll. on Accounting defines an s.r.o. as an accounting entity that is obliged to account for the state and movement of assets, liabilities, revenues, expenses, and the economic result. This core legal regulation determines binding rules for a true and fair view of the corporation’s financial reality.

Violation of this legal norm establishes direct responsibility of the statutory body. The accounting entity must maintain records completely, correctly, demonstrably, and understandably. Financial transactions are recorded in the euro currency and, in the case of foreign currencies, also in the given foreign currency according to the valid exchange rate of the European Central Bank.

Why can an s.r.o. not legislatively utilize single-entry bookkeeping?

Single-entry bookkeeping is an economic system based on the cash principle, which is legislatively reserved primarily for natural persons and specific civic associations. Capital companies cannot utilize it because their financial management requires tracking liabilities and receivables independently of the actual payment execution date.

This state arises from the essence of the accrual principle, where expenses and revenues must be recorded in the period with which they are chronologically and materially related. If a capital company reported its financial management solely based on cash flow, there would be a risk of distorting its solvency and capital adequacy. The legal certainty of business partners and creditors is guaranteed by the transparency provided by comprehensive double-entry bookkeeping.

How to manage bookkeeping in an s.r.o. step by step in 2026?

Systematic management of the corporate agenda includes a continuous process from capturing the initial document, through its material and formal control, up to the final posting to the relevant synthetic and analytical accounts. This exact procedure ensures one hundred percent demonstrability of financial flows and serves as a legislative basis for preparing financial statements.

How does the correct setup of the chart of accounts and opening of books take place?

The chart of accounts of an s.r.o. is an internal regulation containing the synthetic and analytical accounts necessary for a true view of the asset status and economic result. The opening of accounting books on the first day of the accounting period takes place through the initial balance sheet account, whereby balance sheet continuity with the previous period must be maintained.

When establishing a new company, the opening of books is tied to the day of incorporation in the Commercial Register. If the statutory representative forgets the correct setup of analytical records, they then lose track of costs by cost centers or projects. A correctly designed account structure facilitates subsequent internal audit and proving the tax deductibility of expenses.

What are the key obligations of a VAT payer and non-payer when recording documents?

The recording of documents for tax purposes depends on the status of the company according to the Value Added Tax Act. Registration as a VAT payer imposes an obligation on the company to maintain detailed records with an impact on the deduction and payment of tax, while a non-payer tracks turnover and specific cross-border transactions.

If a company exceeds the legally established turnover, it must then obligatorily apply for VAT registration. Non-VAT payers, however, often erroneously assume that this agenda does not concern them at all. When purchasing services from abroad, even a non-payer incurs an obligation to register according to Section 7a of the VAT Act.

Obligation / Parameter | VAT Non-payer (including § 7a) | VAT Payer (§ 4) |

|---|---|---|

Invoicing to customers | Without application of output VAT | Mandatory application of the relevant VAT rate |

Tax deduction from purchases | Not possible (enters expenses) | Full entitlement after fulfilling legal conditions |

Filing of tax returns | Only when the obligation arises (§ 7a) | Monthly or quarterly (tax return + Control Report) |

What are the greatest risks and disadvantages of self-managing the agenda?

Self-managing a double-entry accounting system in a limited liability company carries a high risk of material incorrectness. The absence of professional expertise regarding constantly changing tax legislation generates systemic errors that lead to incorrect reporting of the tax base and subsequent liquidating sanctions.

Many starting entrepreneurs underestimate the complexity of the accrual principle. If tax and non-tax expenses are interchanged, the company exposes itself to a direct risk of additional taxation and penalization. Moreover, self-management robs business owners of time that they could invest in developing the core of their business.

What sanctions are threatened by the Financial Administration for incorrect recording of business transactions?

The Financial Administration sanctions any violation of the Accounting Act and tax regulations based on the severity and duration of the unlawful state. Fines are imposed for incorrect maintenance of accounting books, incomplete reporting of data, or delayed submission of tax returns and financial statements.

If the tax office finds during an audit that the accounting is unprovable, it can then determine the tax using tools, which almost always leads to a disadvantageous recalculation to the detriment of the company.

Is internal accounting or external outsourcing more advantageous for a modern company?

The decision between an internal and external solution depends on the size of the corporation, transactional complexity, and risk management requirements. If a company delegates the accounting agenda to a specialized consulting firm, it then minimizes fixed payroll costs and simultaneously fully transfers legal responsibility for potential methodical errors to the external guarantor.

What are the real economic differences between an employee and a consulting firm?

A comparison of the Total Cost of Ownership (TCO) reveals that an internal department represents a fixed cost burden regardless of seasonal fluctuations in documents. If a company employs an internal accountant, it then covers not only the gross salary but also the employer’s payroll taxes, economic software licenses, continuous professional training, and technical equipment of the workplace.

External outsourcing transforms these fixed expenses into variable costs that exactly copy the actual volume of generated accounting transactions. Furthermore, a professional office has broad team substitutability, which eliminates the risks of downtime during sick leave or vacation use.

How does legal tax optimization affect the reporting of accounting profit?

Legal tax optimization represents a legitimate process of strategic planning that uses available legal tools to minimize the tax burden while maintaining full transparency. If correct methods of deferrals, provisions, and asset depreciation are applied, the company then optimizes cash flow without disrupting its financial rating.

Accounting profit in an s.r.o. is transformed into the tax base through tax-increasing and tax-decreasing items within the meaning of the Income Tax Act. A professional approach consists of setting up processes so that the company displays a healthy economic structure for banking institutions while effectively reducing the effective tax rate.

How does accountant substitution work?

If a company manages its accounting internally and an employee goes on long-term sick leave or resigns, companies often find themselves without relevant coverage or information. In the case of outsourcing, this problem can be easily eliminated, as an accounting firm – including ours – has multiple employees who can back each other up.

Frequently Asked Questions about bookkeeping in an s.r.o. (FAQ)

Can an s.r.o. executive manage bookkeeping on their own without professional education?

Slovak legislation does not explicitly forbid the statutory body from processing the double-entry bookkeeping of their company themselves. However, if the executive decides to self-manage the agenda, they then assume full personal, property, and criminal liability for any discovered shortcomings, whereby the absence of professional knowledge is not accepted as a mitigating circumstance.

What accounting documents must you obligatorily archive and for how long?

According to the Accounting Act, the accounting entity is obliged to retain the financial statements, reports, and accounting documents for a period of 10 years following the year to which they relate. If the company is simultaneously a VAT payer, it must then also respect the provisions of the VAT Act, whereby the transition to a fully digital archive requires meeting the conditions of demonstrability, integrity, and readability of documents.

How does the new legislation in 2026 change the rules for double-entry bookkeeping?

Legislative changes for the year 2026 tighten the conditions of electronic invoicing and introduce advanced mechanisms for automated data exchange with the Financial Administration of the Slovak Republic. If the accounting entity does not implement certified systems for the transformation and validation of data structures, it then risks automatic non-recognition of tax expenses. These reforms require the immediate integration of modern cloud tools and the elimination of manual errors.